Since someone took it upon themselves to sign me up for some sort of MMT “tokenomics” newsletter and I was forced to suffer through reading a dozen paragraphs of nonsense about the utility of value in currencies, I figured I’d share with you all our recent interview on WBD podcast addressing Ms. Kelton’s book.

Inflationary fiscal environments demand continued growth. In fact, they are predicated upon the idea that revenues, income, equity value, debt, and spending will be higher a year from now. These growth expectations are often baked into the markets well in advance, and the Fed’s future fiscal policy is often priced in as well, based on how the markets expect the Fed to react to growth targets, unemployment, and CPI.

As such, inflationary economic paradigms demand growth at all costs. Without growth, massive amounts of liquidity injection and credit expansion are required to prop up stagnanting mal-investment.

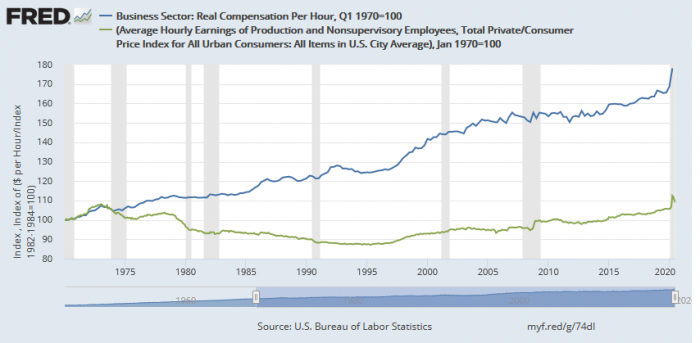

For the acting individual, there is a real cost associated with maintaining the status quo here. That is the effects of diminishing purchasing power at the behest of expansionary monetary policy. In inflationary environments, workers must see their aggregate compensation appreciate, at least as much as the monetary base, or they will end up worse off than they were prior.

Regardless of what any fiat economists might tell you about the purchasing power of a currency being tied to its underlying utility, the economic reality is that as (any) goods become less valuable as they become less scarce, relatively speaking. Printing more money makes the dollar worth less. Period.

Not only is the consumer losing out on the benefits of deflation, if their compensation is not keeping pace with the expansion of the monetary base they are worse off now than they were a year ago in terms of aggregate relative purchasing power. But the problem here is a more complicated than it looks at a glance, and it lies with the ways in which real compensation is calculated.

Thanks to a variety of government policies going all the way back to FDR, tax incentives have created compensatory environments that continually favor compensation in the form of benefits. These benefits often include pension plans, medical coverage, and equity share. For now, let’s just focus on medical benefits.

Legal monopolies created by regulatory capture and compensation in the form of medical benefits have driven healthcare prices through the roof.

As medical care gets more expensive (despite little, if any, real return in the form of better care) the dollar value of your compensation goes up as well! Hot dog! Your now making more money on paper this year than you were last year…except you’re not. Because your pay is still the same, the dollar value of your purchasing power is worth considerably less, and you’re still getting the same healthcare you were before but at a higher price.

Consumers love deflation. Just ask Apple. Imagine if the Apple Emate from 1997 sporting 2 MB of flash memory still cost $800 ($1300 adjusted for inflation) today. Only monetary policy makers and fiat economists have incentive to convince you that the constant erosion of your purchasing power, to bail out failing businesses and prop up bureaucratic spending, is to your benefit.

You will never win in this kind of world unless you cozy up to some central bankers, a strategy it seems the fiat economists have all figured out.

Book of the Month:

The Price of Tomorrow: Why Deflation is the Key to an Abundant Future

-“Every so often, we learn something new that rewrites all of what we have come to know and trust. In those moments, our foundation of knowledge crumbles – and with it, many of the beliefs that we have built on top of it. Those transitions are hard because we do not easily let go of our beliefs.”

WTF1971.com is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to (“WTF1971.com” (amazon.com, or endless.com, MYHABIT.com, SmallParts.com, or AmazonWireless.com).