Some economists have claimed that transitioning away from the Gold Standard under Bretton woods has had no impact on the growth of debt in the current economy. But is this really true?

This claim should be easily falsified, even by the casual observer. But the real question is what allows this continued expansion of debt to continue unhinged? After all, we are (mostly) rational people that live in a rational world. Even the most frivolous of spenders knows that sooner or later living off of borrowed money will end in bankruptcy when the creditors catch on. Why though are governments, particularly the US government able to continue to expand their debt unabated, and further, why do they do this at all?

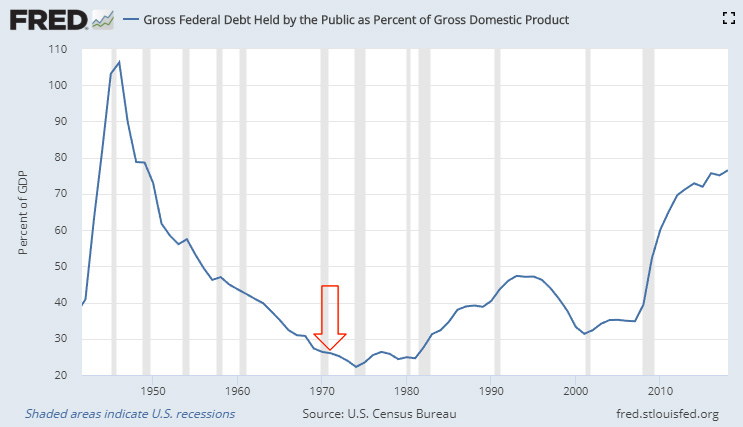

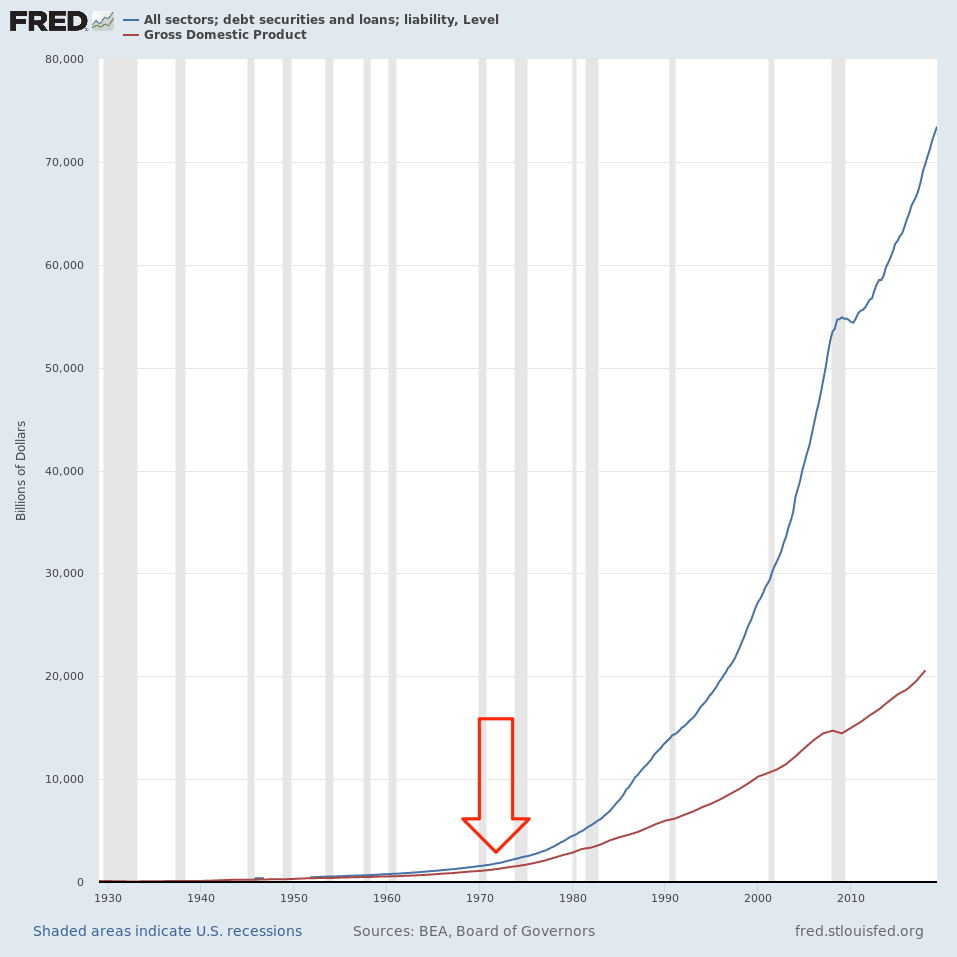

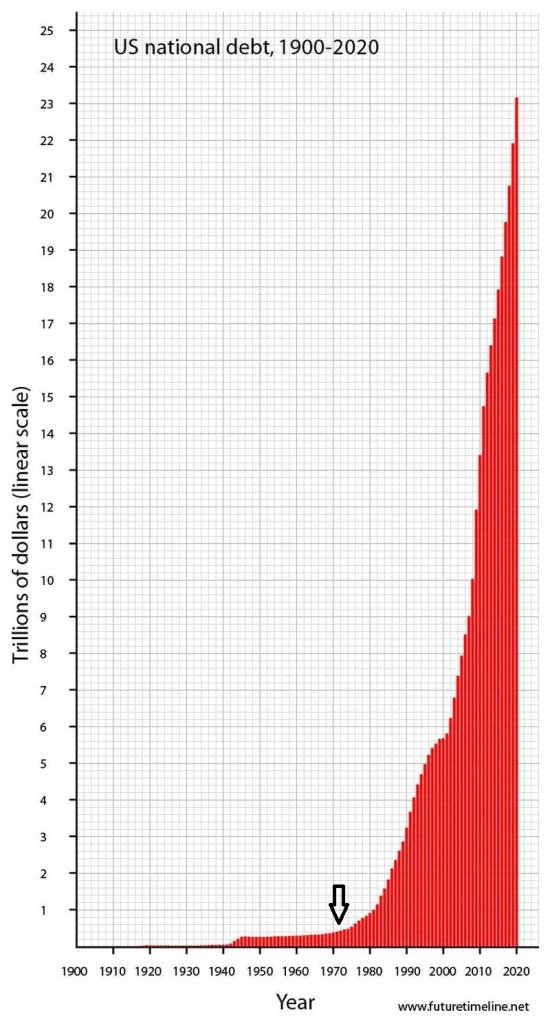

There are two main reasons that we see this continual and unabated debt expansion at the national level. The first and most important factor is the nominal versus real costs of debt. Consider if there were $2 Billion in existence and you had an outstanding debt of $1 Billion. In real terms you owe a considerable amount of the wealth. Now consider if you were to expand the money supply to say $10 Billion but only increase your debt to $2 Billion. Suddenly, even though in nominal terms you’ve only doubled your debt, by a clever accounting trick your debt in real terms has gone from 50% (2 billion: 1 billion) of the outstanding currency to 20% (10 billion: 2 billion). This example is purposefully hyperbolic to more clearly demonstrate the effects.

Ordinarily, debt not used in profitable speculation would be considered mal-investment, and either forced into liquidation or be paid for using the debtors assets. But this is conveniently not so with a lender of last resort (The Federal Reserve and the IMF).

Remembering what we know about The Cantillon Effect, and from how we’ve seen as the Fed acting as a lender of last resort for the privileged few, it’s not difficult to discern here how governments and their cohorts double dip on currency printing and debt expansion. By being the first to spend newly printed currency, and continuing to increase nominal spending while bringing those relative debt servicing costs down in real terms, what is the incentive not to continue to ride this wave?

An important consequence of this debt expansion strategy, however, is a rising cost in annual debt servicing, required on outstanding debts. Year over year, this continually makes up a larger percentage of the Federal Budget. One way or another, this disparity must be made up for by either raising taxes or more debt and monetary expansion.

The second and perhaps equally important factor of debt and spending expansion in the public sector is political popularity. Politicians who cut expenses, even to horribly failing business models or unproductive aspects of society seek only to lose favor with those corresponding groups. In a democratic society (or a even in a republic such as the USA) a politician is incentivized to appeal to as broad of a range of demographics as possible, this is particularly exacerbated by the two party false dichotomy seen in most countries. A politician’s most powerful tool when seeking election or reelection is to guarantee the allocation of capital to special interests. Rarely is cutting expenses ever politically popular on a net basis.

In future newsletters we will also delve into the revolving door of Washington DC and the Wall Street, to see how these incentives align even further.

Book of the Month:

The Dao of Capital: Austrian Investing in a Distorted World

-“Although the future remains uncertain, the entrepreneur relies on “specific anticipative understanding,” which “can be neither taught nor learned”; he does not focus on what was or is, but acts upon what he expects the future to be.”

WTF1971.com is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to (“WTF1971.com” (amazon.com, or endless.com, MYHABIT.com, SmallParts.com, or AmazonWireless.com).