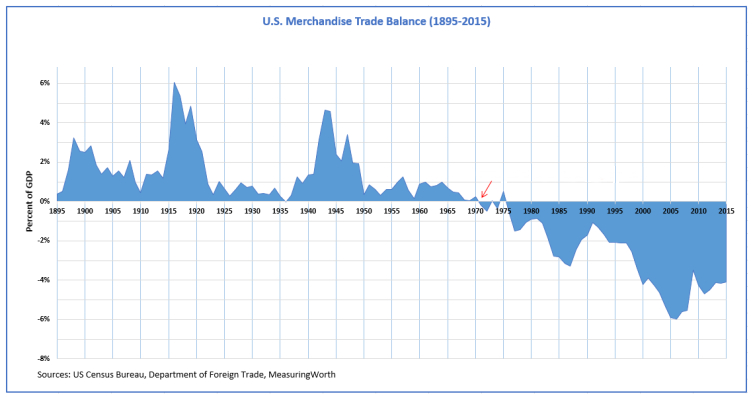

The Triffin Dilemma (AKA Triffin Paradox) is a situation of conflicting interest in economic policy when it comes to global reserve currencies. Aptly named after the Belgian-American economist Robert Triffin, the Triffin dilemma recognizes that in order to fulfill global demand for a reserve currency, its issuing nation must maintain a trade deficit in order to export a sufficient supply of its currency. Here’s a familiar visual.

Notice the dramatic shift in trade good balance during our favorite year, which has continued to increase in magnitude ever since. Certainly all the punditry about “fixing the US trade deficit” is little more than a pipe dream under the current paradigm. This dilemma is actually why the late John Maynard Keynes had advocated for an independent sovereign reserve currency called the “Bancor” at the Bretton Woods conference in 1944.

In our current economic paradigm the primary global reserve currency is the USD, followed by the Euro (other notable mentions include the Japanese Yen, the Chinese Yuan, the Swiss Franc, and the Canadian Dollar). As we know, the USD supplanted itself as the global reserve currency via the Bretton Woods agreement, as the USD was pegged gold held in the US treasury and all other national currencies falling under the Bretton Woods system were pegged to the USD. Before the USD was the de-facto global reserve currency it was the British Sterling Pound (which fell from grace following the UK’s WW1 and WW2 debt accrual), and before that it was the Dutch Guilder.

As we know well by now, the Triffin Dilemma was largely the driving factor in the destabilization of the Bretton Woods system, as the number of dollars in circulation to meet global reserve currency demand exceeded the amount of gold held by the US treasury. In hindsight this actually makes the idea of sovereign nation state currencies pegged to a reserve currency (which is also a nation state currency), which is in turn pegged to a commodity seem a little more than absurd.

The problem with the Bancor proposed by Keynes is how to maintain the independence of a global sovereign reserve currency without overly complicated international banking institutions and a highly centralized governance model.

Interestingly, the St. Louis Fed commented on this exact concept in 2018. Perhaps a new paradigm is on the horizon.

Book of the Month:

The Dao of Capital: Austrian Investing in a Distorted World

-“Although the future remains uncertain, the entrepreneur relies on “specific anticipative understanding,” which “can be neither taught nor learned”; he does not focus on what was or is, but acts upon what he expects the future to be.”

WTF1971.com is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to (“WTF1971.com” (amazon.com, or endless.com, MYHABIT.com, SmallParts.com, or AmazonWireless.com).